Re: [Gretl-users] Nonlinear switching regression vs Loop constructs

Thank you for your reply Allin. The question about the dependent

variable is now cleared.

Minor adjustments were made to the script to save the models seperately.

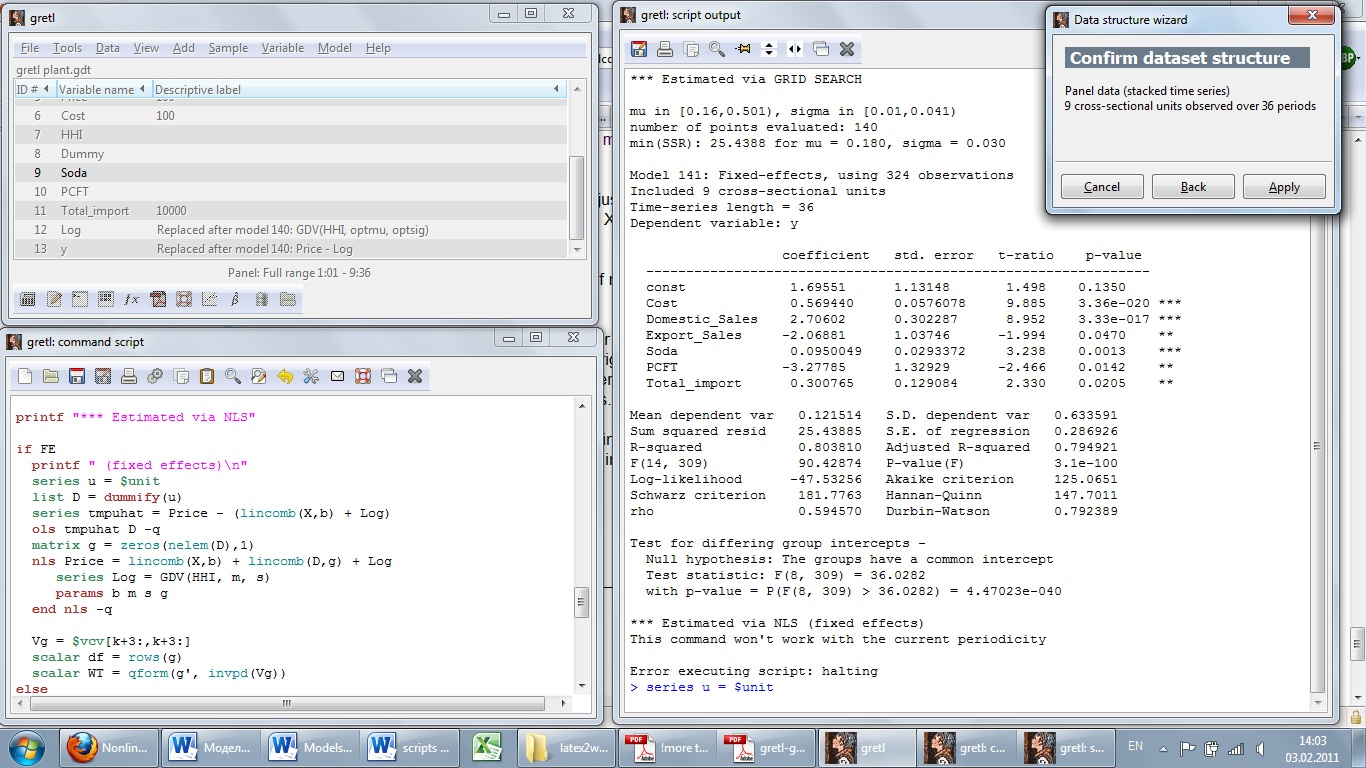

However the problem with $unit in the script still persists despite

the dataset structure set as panel. Please see the attached screenshot

and the script file.

My question about the NLS procedure is more theoretical - imho the

manual doesn't provide enough theoretical background for the way the

Gauss-Newton regression is used

Best regards,

Gregory

On Thu, Feb 3, 2011 at 3:20 AM, Allin Cottrell <cottrell(a)wfu.edu> wrote:

On Tue, 1 Feb 2011, GREg Ory wrote:

> First of all I would like to express most sincere thanks to everybody

> who answered on the matter. All gretl users must have seen this very

> fine result of scripting and it’s rare to receive fast and quality

> help and get exactly what you were looking for when dealing with

> econometric packages. Allin and Jack – I may become your fan.

[...]

> A question: why estimate ‘y – GDV’ and not ‘y’ as a dependent

> variable. I understand that it’s equivalent in the linear regression

> just want to know the reason for this.

The coefficient on the variable constructed by Jack's GDV()

function is constrained to be 1.0 in the model you're estimating.

So the obvious way of implementing this is to subtract it from the

"real" dependent variable.

> The problem with the script is - NLS isn't estimated if FE = 1

> because series u = $unit doesn't work with the current

> periodicity. Some pointers on how to solve this would be nice.

Apparently your dataset is not recognized as a panel. See the

"setobs" command, or the menu item /Data/Dataset structure in the

GUI.

> Another problem I encountered is my little knowledge of the NLS

> estimation process – I can’t figure out how Jack uses linear

> combinations, nelem function and covarince matrix to get the NLS

> results.

The lincomb() (linear combination) function is just a way of doing

the matrix mutiplication X*b, in the case where X is not actually

a matrix but a list of series.

The nelem() function just returns the number of members in a list

of series.

In gretl's nls you need to construct a formula for the dependent

variable -- in terms of various parameters and right-hand-side

variables -- then tell gretl what are the parameters you want to

adjust to minimize the sum of squared residuals.

The model you wanted to estimate is basically linear (hence the

"lincomb" part), with an element of nonlinearity introduced by the

logistic term (hence the need for nls).

Allin Cottrell

_______________________________________________

Gretl-users mailing list

Gretl-users(a)lists.wfu.edu

http://lists.wfu.edu/mailman/listinfo/gretl-users

Attachments:

- nonlin_problem.jpg (image/jpeg — 367.6 KB)

- nonlin2.4.inp (application/octet-stream — 3.2 KB)

{kind=link}