[Gretl-users] State space with three time-variant coefficients

Dear All,

I'm in trouble with state space models, as I find them difficult to implement. I was

able to set up a few with just one time-variant unobservable variable but I'm not sure

on what I'm doing when there are more. Let's say we depart from the example of the

Phillips curve on pages 345-346 of Gretl manual, where the inflation rate (INFQ) depends

on the unemployment rate (URX). In the example, the intercept is time-invariant and the

coefficient for URX follows a random walk.

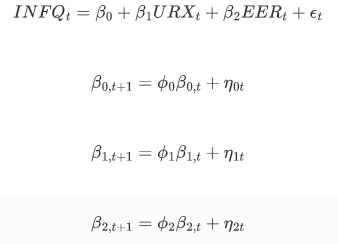

Let's expand the model such that there is a second independent variable Effective

Exchange Rate (EER) explaining INFQ. Additionally, I want all three coefficients to follow

an AR(1) process. The image attached shows this new model. How hard would that be to

implement these changes on the script depicted on manual page 347 (as follows):

<hansl>

function void at_each_step(bundle *b)

b.obsymat = transp(b.mX[b.t,])

end function

open AWM.gdt --quiet

smpl 1974:1 1994:1

/* parameter initialization */

scalar b0 = mean(INFQ)

scalar s_obs = 0.1

scalar s_state = 0.1

/* bundle setup */

bundle B = ksetup(INFQ, 1, 1, 1)

matrix B.mX = {URX}

matrix B.depvar = {INFQ}

B.timevar_call = "at_each_step"

B.diffuse = 1

/* ML estimation of intercept and the two variances */

mle LL = err ? NA : B.llt

B.obsy = B.depvar - b0

B.obsvar = s_obs^2

B.statevar = s_state^2

err = kfilter(&B)

params b0 s_obs s_state

end mle

/* display the smoothed time-varying slope */

ksmooth(&B)

series tvar_b1hat = B.state[,1]

series tvar_b1se = sqrt(B.stvar[,1])

gnuplot tvar_b1hat --time-series --with-lines --output=display \

--band=tvar_b1hat,tvar_b1se,1.96 --band-style=fill

</hansl>

--

F.R.Costa

Attachments:

- attachment.htm (text/html — 2.8 KB)

- Screenshotat2021-10-0717-40-08.png (image/png — 14.1 KB)

{kind=link}