11:10 p.m.

Please yr help with this issue

After performing a simple Linear regression (file attached) and asking for

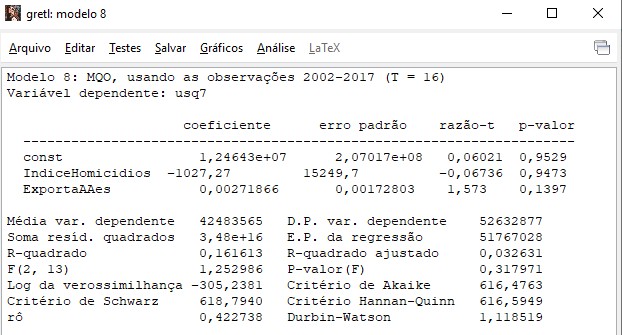

a Breush Pagan Heterocedasticity test in Menu TEST I get the response below

[image: image.png]

Instead if square residual are saved and used as a Dependent variable

against above regressors the answer is different, please see below

[image: image.png]

Why does it happen?

please, I am waiting for your Help and advise

best regrards

{kind=link}

{kind=link}

1:03 p.m.

On Sat, 13 Jun 2020, Salvatore Salvo wrote:

Please yr help with this issue

After performing a simple Linear regression (file attached) and asking for

a Breush Pagan Heterocedasticity test in Menu TEST I get the response below

Instead if square residual are saved and used as a Dependent variable

against above regressors the answer is different, please see below

Why does it happen?

In the Breusch-Pagan test (T. S. Breusch and A. R. Pagan,

Econometrica 47/5, 1979), the dependent variable in the auxiliary

regression is the squared residual scaled by the ML estimate of its

variance:

series g = $uhat^2 / ($ess/$T)

Regress this on the relevant regressors and you will reproduce

gretl's test. The LM test statistic is half of the Regression (or

"Explained") sum of squares. After running the auxiliary regression

you can find it as

LM = (sst(g) - $ess) / 2

Here's a complete example:

open data4-10

ols ENROLL 0 CATHOL INCOME

modtest --breusch-pagan

series g = $uhat^2 / ($ess/$T)

ols g 0 CATHOL INCOME --simple-print

LM = (sst(g) - $ess) / 2

Allin Cottrell

2:48 a.m.

OK, this is more interesting than I thought (and I'd welcome

comments/criticism from others).

Salvatore's question is prompted by a difference in results between

gretl's Breusch-Pagan test for heteroskedasticity (via the command

modtest --breusch-pagan) and the test as implemented in Eviews.

First point: on the face of it there's a difference between the test

actually proposed by Breusch and Pagan (Econometrica, 1979), which

I'll call Test1, and that performed in Eviews, which I'll call

Test2. (Eviews is by no means alone in using Test2, it's also the

one described in the Wikipedia entry.) Both tests involve auxiliary

regressions estimated via OLS, with the same set of independent

variables, but

* In Test1 the dependent variable is the squared residual from the

original regression divided by the ML estimator of the error

variance for that regression, and the LM test statistic is half of

the explained sum of squares from the auxiliary regression. (This is

very clearly set out on the first page of the B-P paper.)

* In Test2 the dependent variable is the (unscaled) squared residual

from the original regression and the LM test statistic is sample

size times R^2 from the auxiliary regression.

At first I thought this difference might be merely apparent (that

is, the results should be numerically identical if done right). But

I couldn't prove that and (unless I've messed up) simulation shows

that they're not at all numerically identical. (Maybe they're

asymptotically equivalent?) In that case, which one is "right" or

"better"?

Monte Carlo to the rescue. I show my test script below. It can be

run in two modes, depending on the value of "H0_true" near the top

of the script.

* If H0_true = 1 the simulated error is homoskedastic and the

rejection rates for the two tests give a measure of their sizes. I'm

using the 5 percent significance level, so ideally the empirical

rejection rate should be close to 0.05.

* If H0_true = 0 the simulated error is by construction

heteroskedastic and the rejection rates give a measure of power.

On running the script in both modes several times, here's what I

see:

* Size: both tests seem about right. Sometimes one is closer to the

nominal size of 0.05, sometimes the other.

* Power: Test1 (the original) seems to be substantially better.

Here are rejection rates from a few runs:

H0_true = 1

Test1 0.049, Test2 0.053

Test1 0.043, Test2 0.046

Test1 0.048, Test2 0.047

H0_true = 0

Test1 0.548, Test2 0.311

Test1 0.546, Test2 0.316

Test1 0.698, Test2 0.520

If anyone sees an error in my simulation, please let me know!

<hansl>

set verbose off

# sample size for regressions

nulldata 100

# uncomment below for reproducible results

# set seed 76543

# error term is homoskedastic?

H0_true = 1

# independent variable

series x = normal()

# 5 percent critical value for chi-square(1)

scalar X1crit = critical(X, 1, 0.05)

# number of replications

K = 5000

# recorders

matrix reject = zeros(1,2)

matrix LMdiff = zeros(K,1)

loop i=1..K --quiet

e = normal()

if H0_true

# homoskedastic

y = 10 + x + e

else

# heteroskedastic

y = 10 + x + 0.2*x*e

endif

# estimate original regression

ols y 0 x --quiet

u2 = $uhat^2

# Test1: as Breusch and Pagan (1979)

vml = $ess / $T

g = u2/vml

ols g 0 x --quiet

LM1 = (sst(g) - $ess)/2

reject[1] += LM1 > X1crit

# Test2: as Wikipedia, Eviews

ols u2 0 x --quiet

LM2 = $trsq

reject[2] += LM2 > X1crit

LMdiff[i] = LM1 - LM2

endloop

reject /= K

printf "Rejection rates at 5 percent level:\n"

printf " Test1 %.3f, Test2 %.3f\n", reject[1], reject[2]

colnames(LMdiff, "LMdiff")

summary --matrix=LMdiff --simple

</hansl>

Allin

8:46 a.m.

Am 14.06.2020 um 17:48 schrieb Allin Cottrell:

OK, this is more interesting than I thought (and I'd welcome

comments/criticism from others).

Salvatore's question is prompted by a difference in results between

gretl's Breusch-Pagan test for heteroskedasticity (via the command

modtest --breusch-pagan) and the test as implemented in Eviews.

First point: on the face of it there's a difference between the test

actually proposed by Breusch and Pagan (Econometrica, 1979), which I'll

call Test1, and that performed in Eviews, which I'll call Test2.

This old thread from the Stata forum might be relevant:

https://www.stata.com/statalist/archive/2006-04/msg00076.html

So maybe power turns around for non-Gaussian scenarios.

cheers

sven

12:44 p.m.

On Sun, 14 Jun 2020, Sven Schreiber wrote:

Am 14.06.2020 um 17:48 schrieb Allin Cottrell:

> OK, this is more interesting than I thought (and I'd welcome

> comments/criticism from others).

>

> Salvatore's question is prompted by a difference in results between

> gretl's Breusch-Pagan test for heteroskedasticity (via the command

> modtest --breusch-pagan) and the test as implemented in Eviews.

>

> First point: on the face of it there's a difference between the test

> actually proposed by Breusch and Pagan (Econometrica, 1979), which I'll

> call Test1, and that performed in Eviews, which I'll call Test2.

This old thread from the Stata forum might be relevant:

https://www.stata.com/statalist/archive/2006-04/msg00076.html

So maybe power turns around for non-Gaussian scenarios.

Certainly relevant; thanks, Sven. I hadn't twigged that "Test2" is

equivalent to Koenker's robust B-P version. I re-ran my test script

with uniform errors (should probably try some other cases) and

found:

* Under H0 the original B-P test is "under-sized": rejects at much

less than 5 percent frequency using alpha = 0.05. The size of the

robust version is roughly right.

* Under my H1, error=0.2*x*uniform(), the original B-P test still

rejects with much higher frequency than the Koenker variant.

Allin

5:07 a.m.

Am 15.06.2020 um 03:44 schrieb Allin Cottrell:

On Sun, 14 Jun 2020, Sven Schreiber wrote:

> So maybe power turns around for non-Gaussian scenarios.

Certainly relevant; thanks, Sven. I hadn't twigged that "Test2" is

equivalent to Koenker's robust B-P version. I re-ran my test script with

uniform errors (should probably try some other cases) and found:

* Under H0 the original B-P test is "under-sized": rejects at much less

than 5 percent frequency using alpha = 0.05. The size of the robust

version is roughly right.

* Under my H1, error=0.2*x*uniform(), the original B-P test still

rejects with much higher frequency than the Koenker variant.

Obviously, if the original test were always correctly sized or

conservative _and_ had more power, it would be superior. My suspicion is

that for other kinds of violations of the assumptions it might be

oversized, however. But I don't know this specific literature, so far as

it exists.

cheers

sven

5:22 a.m.

On Mon, 15 Jun 2020, Sven Schreiber wrote:

Am 15.06.2020 um 03:44 schrieb Allin Cottrell:

> On Sun, 14 Jun 2020, Sven Schreiber wrote:

>> So maybe power turns around for non-Gaussian scenarios.

>

> Certainly relevant; thanks, Sven. I hadn't twigged that "Test2" is

> equivalent to Koenker's robust B-P version. I re-ran my test script with

> uniform errors (should probably try some other cases) and found:

>

> * Under H0 the original B-P test is "under-sized": rejects at much less

> than 5 percent frequency using alpha = 0.05. The size of the robust

> version is roughly right.

>

> * Under my H1, error=0.2*x*uniform(), the original B-P test still

> rejects with much higher frequency than the Koenker variant.

Obviously, if the original test were always correctly sized or

conservative _and_ had more power, it would be superior. My suspicion is

that for other kinds of violations of the assumptions it might be

oversized, however. But I don't know this specific literature, so far as

it exists.

I tried another run of my Monte Carlo, with t(12) errors. Original

B-P was somewhat oversized (around 0.075 or 0.08 for nominal 0.05)

but reasonably powerful. The Koenker robust variant was correctly

sized at 0.05 (as claimed) but had about 1/2 to 5/8 the power

against my H1 (with error multiplied by 0.2*x).

It seems the subsequent literature has kind of skated over Koenker's

1981 caveat, that the statistic is "not entirely satisfactory" since

"the power of the resulting test may be quite poor except under

idealized Gaussian conditions". I would add, _even_ under Gaussian

conditions.

Allin

8:34 a.m.

Am 15.06.2020 um 20:22 schrieb Allin Cottrell

I tried another run of my Monte Carlo, with t(12) errors. Original

B-P

was somewhat oversized (around 0.075 or 0.08 for nominal 0.05) but

reasonably powerful. The Koenker robust variant was correctly sized at

0.05 (as claimed) but had about 1/2 to 5/8 the power against my H1 (with

error multiplied by 0.2*x).

Well if you size-adjust the first test by multiplying with 0.05/0.08 you

also arrive at 5/8 of the raw power. So maybe not so different.

It seems the subsequent literature has kind of skated over

Koenker's

1981 caveat, that the statistic is "not entirely satisfactory" since

"the power of the resulting test may be quite poor except under

idealized Gaussian conditions". I would add, _even_ under Gaussian

conditions.

So what about Wooldridge's F version? It uses the same auxiliary

regression as Koenker and simply takes the ordinary F statistic from

that. Although I fail to see why that would have more power, but who knows.

cheers

sven

2242

days inactive

2244

days old

7 comments

3 participants

participants (3)

-

Allin Cottrell

Allin Cottrell -

Salvatore Salvo

Salvatore Salvo -

Sven Schreiber

Sven Schreiber