3:35 p.m.

Hello all,

Why does this model generate different outcomes, even if the same variables

and specification are been used? There is just a change in the position of

the variables.

Many thanks,

Bruno

{kind=link}

{kind=link}

3:42 p.m.

Am 04.10.2012 17:35, schrieb Bruno Thiago Tomio:

Hello all,

Why does this model generate different outcomes, even if the same

variables and specification are been used? There is just a change in

the position of the variables.

yhat1 <> logarea -> different results

Many thanks,

Bruno

_______________________________________________

Gretl-users mailing list

Gretl-users(a)lists.wfu.edu

http://lists.wfu.edu/mailman/listinfo/gretl-users

6:53 p.m.

New subject: RES: Same model, different position of variables, different results

Sorry, I did not get it, Pindar. Could you please be more specific?

De: gretl-users-bounces(a)lists.wfu.edu

[mailto:gretl-users-bounces@lists.wfu.edu] Em nome de Pindar

Enviada em: quinta-feira, 4 de outubro de 2012 12:42

Para: Gretl list

Assunto: Re: [Gretl-users] Same model, different position of variables,

different results

Am 04.10.2012 17:35, schrieb Bruno Thiago Tomio:

Hello all,

Why does this model generate different outcomes, even if the same variables

and specification are been used? There is just a change in the position of

the variables.

yhat1 <> logarea -> different results

Many thanks,

Bruno

_______________________________________________

Gretl-users mailing list

Gretl-users(a)lists.wfu.edu

http://lists.wfu.edu/mailman/listinfo/gretl-users

7:01 p.m.

New subject: RES: Same model, different position of variables, different results

Am 04.10.2012 20:53, schrieb Bruno Thiago Tomio:

Sorry, I did not get it, Pindar. Could you please be more specific?

I know just enough Portuguese (and also know gretl's messages...) to see

that you have an exact collinearity problem, so gretl drops some

arbitrary variables, and this arbitrary choice depends on the ordering.

Or is there more to it? If so, please show us something without the rank

deficiency.

cheers,

sven

7:05 p.m.

New subject: RES: Same model, different position of variables, different results

Probably gretl is discarding the first variable found to be colinear.

So yhat1 is colinear to logarea. When you exchange the position, you

get a diferent set.

Hélio

On Thu, Oct 4, 2012 at 7:53 PM, Bruno Thiago Tomio

<brunottomio(a)yahoo.com.br> wrote:

Sorry, I did not get it, Pindar. Could you please be more specific?

De: gretl-users-bounces(a)lists.wfu.edu

[mailto:gretl-users-bounces@lists.wfu.edu] Em nome de Pindar

Enviada em: quinta-feira, 4 de outubro de 2012 12:42

Para: Gretl list

Assunto: Re: [Gretl-users] Same model, different position of variables,

different results

Am 04.10.2012 17:35, schrieb Bruno Thiago Tomio:

Hello all,

Why does this model generate different outcomes, even if the same variables

and specification are been used? There is just a change in the position of

the variables.

yhat1 <> logarea -> different results

Many thanks,

Bruno

_______________________________________________

Gretl-users mailing list

Gretl-users(a)lists.wfu.edu

http://lists.wfu.edu/mailman/listinfo/gretl-users

_______________________________________________

Gretl-users mailing list

Gretl-users(a)lists.wfu.edu

http://lists.wfu.edu/mailman/listinfo/gretl-users

10:30 p.m.

New subject: RES: Same model, different position of variables, different results

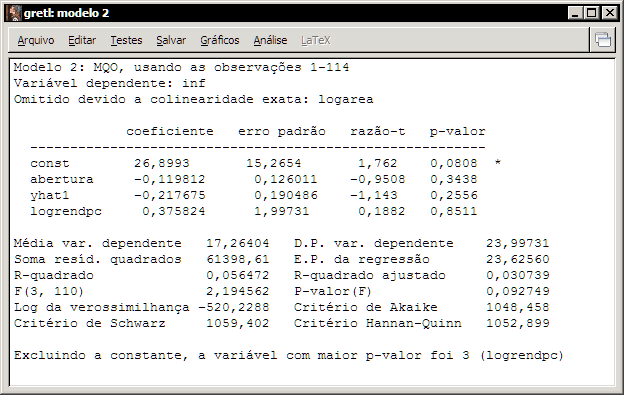

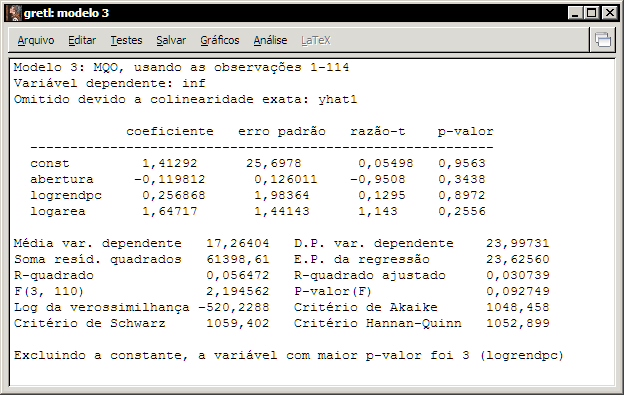

Dear Bruno,

The problem is simple: the variable "logarea" is not equal to

"yhat1".

logarea yhat1

1 13.73169 17.32861

2 13.88510 16.59191

3 14.90278 9.24835

4 10.38514 43.42590

5 5.48064 80.59877

6 10.92590 37.84531

...

Um abraço,

Henrique

1:12 p.m.

New subject: RES: Same model, different position of variables, different results

Dear Bruno,

It seems that you are running a regresion with boht logarea and yhat1,

however, gretl drops one of the variable because they collinear. That is

right given that correlation is 99.93%

abertura logrendpc logarea yhat1

1.0000 0.1402 -0.6693 0.6698 abertura

1.0000 -0.1715 0.2093 logrendpc

1.0000 -0.9993 logarea

1.0000 yhat1

Now, your question is why you have a different dropped variable if you

change the order of the regressors, right? I am not sure why that is the

case, but it happens also in other packages. I remember similar issue in

Stata, when you have a different dropped variable if you use a different

command, but forcing to apply the same procedure. For example comparing OLS

con IV (but with trivial instruments).

Although, I don't have the question I think is not a serious problem. If 2

variables are highly correlated then any of those can be used. Indeed, many

times you could cut down your regressor into principal components to avoid

collinearity. Moreover, yhat1 is predicted variable from a previous model

and it is likely that logarea (or some similar variable) is a relevant in

that model.

Best, Rodrigo.

2012/10/4 Henrique Andrade <henrique.coelho(a)gmail.com>

Dear Bruno,

The problem is simple: the variable "logarea" is not equal to

"yhat1".

logarea yhat1

1 13.73169 17.32861

2 13.88510 16.59191

3 14.90278 9.24835

4 10.38514 43.42590

5 5.48064 80.59877

6 10.92590 37.84531

...

Um abraço,

Henrique

_______________________________________________

Gretl-users mailing list

Gretl-users(a)lists.wfu.edu

http://lists.wfu.edu/mailman/listinfo/gretl-users

1:40 p.m.

New subject: RES: RES: Same model, different position of variables, different results

Dear all,

Thank you very much for your replies (Rodrigo, Sven and Henrique).

This was part of an exogeneity test. When the variable yhat1 was excluded,

the test does not work. But when one rearrange the model in a way that yhat1

is not placed at the end, the test is possible (i.e. gretl excludes logarea

instead of yhat1, due to the collinearity problem).

Best,

Bruno

De: gretl-users-bounces(a)lists.wfu.edu

[mailto:gretl-users-bounces@lists.wfu.edu] Em nome de Rodrigo Alfaro

Arancibia

Enviada em: sexta-feira, 5 de outubro de 2012 10:12

Para: Gretl list

Assunto: Re: [Gretl-users] RES: Same model, different position of variables,

different results

Dear Bruno,

It seems that you are running a regresion with boht logarea and yhat1,

however, gretl drops one of the variable because they collinear. That is

right given that correlation is 99.93%

abertura logrendpc logarea yhat1

1.0000 0.1402 -0.6693 0.6698 abertura

1.0000 -0.1715 0.2093 logrendpc

1.0000 -0.9993 logarea

1.0000 yhat1

Now, your question is why you have a different dropped variable if you

change the order of the regressors, right? I am not sure why that is the

case, but it happens also in other packages. I remember similar issue in

Stata, when you have a different dropped variable if you use a different

command, but forcing to apply the same procedure. For example comparing OLS

con IV (but with trivial instruments).

Although, I don't have the question I think is not a serious problem. If 2

variables are highly correlated then any of those can be used. Indeed, many

times you could cut down your regressor into principal components to avoid

collinearity. Moreover, yhat1 is predicted variable from a previous model

and it is likely that logarea (or some similar variable) is a relevant in

that model.

Best, Rodrigo.

11:31 a.m.

New subject: Signs and Interval of Error Corrections Terms in within a VECM framework

Hi All,

I understand within a bivariate VECM framework, the Error Correction

Terms(ECTs) have to be negative and situated within the interval: 0 and -1. Does this

principle on sign and interval apply to a multivariate VECM framework?

Cheers

6:34 p.m.

New subject: Signs and Interval of Error Corrections Terms in within a VECM framework

Dear Asongu,

In Vinod, H.D. (2008)'s "Hands-on Intermediate Econometrics Using R", in

sections 3.4.2 to 3.4.5 I've found some hints for your question. The author

uses a bivariate ECM. If you consider no a priori knowledge for the

relationship between, say, x and y, so we have a system of two equations,

both with ECM's.

In this case, says the author: "If the equilibrium error experienced by

economic agent at time t-1 is positive, in inequality (yt-1 > bxt-1) must

hold. During the current period t decreasing the left-hand side (yt < yt-1

or deltayt < 0) and increasing the right-hand side (bxt > bxt-1, deltaxt >

0, since b >0) of the inequality reduces the equilibrium error. If the

agent learns from past errors in predictable ways, we have seen that this

implications on the signs of coefficients in [number of equation] implying

nonrejection of two hypothesis, gama1 > 0 and gama2 <0".

Gama1 and 2 are, respectively, the coefficients of the long-run

relationship in t-1 (as usual in VECM). The gama 1 is for delta xt's

equation and the gama 2 for the delta yt's one).

So, in this case, you should expect a positive coefficient for the

coefficient. Is that what you asked? Hope to have helped you.

Best Wishes,

Claudio D. Shikida

http://www.shikida.net and http://works.bepress.com/claudio_shikida/

Esta mensagem pode conter informação confidencial e/ou privilegiada. Se

você não for o destinatário ou a pessoa autorizada a receber esta mensagem,

não poderá usar, copiar ou divulgar as informações nela contidas ou tomar

qualquer ação baseada nessas informações. Se você recebeu esta mensagem por

engano, por favor avise imediatamente o remetente, respondendo o presente

e-mail e apague-o em seguida.

This message may contain confidential and/or privileged information. If you

are not the addressee or authorized to receive this for the addressee, you

must not use, copy, disclose or take any action based on this message or

any information herein. If you have received this message in error, please

advise the sender immediately by reply e-mail and delete this message.

On Sat, Oct 13, 2012 at 8:31 AM, Anutechia Asongu

<simplice_peace(a)yahoo.com>wrote:

Hi All,

I understand within a bivariate VECM framework, the Error

Correction Terms(ECTs) have to be negative and situated within the

interval: 0 and -1. Does this principle on sign and interval apply to a

multivariate VECM framework?

Cheers

_______________________________________________

Gretl-users mailing list

Gretl-users(a)lists.wfu.edu

http://lists.wfu.edu/mailman/listinfo/gretl-users

11:35 a.m.

New subject: Signs and Interval of Error Corrections Terms in within a VECM framework

Hi

I would not say that the ECT terms have to be between 0 and -1. it was not

clear to me whether you are referring to the cointegrating parameters (the

betas) or the speed adjustment (alphas)? For the betas, the values from

these vectors can take any value, but need to be normalised for

identification purpose.

For the alphas, the expected sign depends precisely on the corresponding

value in the cointegrating vector. The reasoning in the bi-variate case can

be simply extended to the k-variate. Taking a vector: y= b1 x - b2z, (with

b1 and b2 positive):

With a positive shocks, so that y > b1 x - b2z, if variables are "error

correcting" you expect:

-y to have negative alpha coefficient (should decrease the y to "reduce"

the inequality by reducing the left)

-x to have a positive coefficient (should increase the x in order to

"reduce" the inequality by increasing the right)

-z to have a negative coefficient (should increase the z in order to

"reduce" the inequality by increasing the right)

So I do not think one can say that the values should be bezween 0 and -1.

Best

Matthieu

2012/10/15 Claudio Shikida (敷田治誠 クラウジオ) <cdshikida(a)gmail.com>

Dear Asongu,

In Vinod, H.D. (2008)'s "Hands-on Intermediate Econometrics Using R", in

sections 3.4.2 to 3.4.5 I've found some hints for your question. The author

uses a bivariate ECM. If you consider no a priori knowledge for the

relationship between, say, x and y, so we have a system of two equations,

both with ECM's.

In this case, says the author: "If the equilibrium error experienced by

economic agent at time t-1 is positive, in inequality (yt-1 > bxt-1) must

hold. During the current period t decreasing the left-hand side (yt < yt-1

or deltayt < 0) and increasing the right-hand side (bxt > bxt-1, deltaxt >

0, since b >0) of the inequality reduces the equilibrium error. If the

agent learns from past errors in predictable ways, we have seen that this

implications on the signs of coefficients in [number of equation] implying

nonrejection of two hypothesis, gama1 > 0 and gama2 <0".

Gama1 and 2 are, respectively, the coefficients of the long-run

relationship in t-1 (as usual in VECM). The gama 1 is for delta xt's

equation and the gama 2 for the delta yt's one).

So, in this case, you should expect a positive coefficient for the

coefficient. Is that what you asked? Hope to have helped you.

Best Wishes,

Claudio D. Shikida

http://www.shikida.net and http://works.bepress.com/claudio_shikida/

Esta mensagem pode conter informação confidencial e/ou privilegiada. Se

você não for o destinatário ou a pessoa autorizada a receber esta mensagem,

não poderá usar, copiar ou divulgar as informações nela contidas ou tomar

qualquer ação baseada nessas informações. Se você recebeu esta mensagem por

engano, por favor avise imediatamente o remetente, respondendo o presente

e-mail e apague-o em seguida.

This message may contain confidential and/or privileged information. If

you are not the addressee or authorized to receive this for the addressee,

you must not use, copy, disclose or take any action based on this message

or any information herein. If you have received this message in error,

please advise the sender immediately by reply e-mail and delete this

message.

On Sat, Oct 13, 2012 at 8:31 AM, Anutechia Asongu <

simplice_peace(a)yahoo.com> wrote:

>

> Hi All,

> I understand within a bivariate VECM framework, the Error

> Correction Terms(ECTs) have to be negative and situated within the

> interval: 0 and -1. Does this principle on sign and interval apply to a

> multivariate VECM framework?

> Cheers

>

>

> _______________________________________________

> Gretl-users mailing list

> Gretl-users(a)lists.wfu.edu

> http://lists.wfu.edu/mailman/listinfo/gretl-users

>

_______________________________________________

Gretl-users mailing list

Gretl-users(a)lists.wfu.edu

http://lists.wfu.edu/mailman/listinfo/gretl-users

12:25 p.m.

New subject: Signs and Interval of Error Corrections Terms in within a VECM framework

Am 16.10.2012 13:35, schrieb Matthieu Stigler:

So I do not think one can say that the values should be bezween 0 and -1.

This statement is correct. But please forgive me that I'm not going to

contribute to this non gretl-specific discusson apart from this

reaction. (Which doesn't mean that I necessarily want you to stop the

discussion, but I would recommend that the interested people study the

textbook literature as well/instead/first.)

cheers,

sven

4933

days inactive

4945

days old

11 comments

9 participants

participants (9)

-

Anutechia Asongu

Anutechia Asongu -

Bruno Thiago Tomio

Bruno Thiago Tomio -

Claudio Shikida (敷田治誠 クラウジオ)

Claudio Shikida (敷田治誠 クラウジオ) -

Henrique Andrade

Henrique Andrade -

Hélio Guilherme

Hélio Guilherme -

Matthieu Stigler

Matthieu Stigler -

Pindar

Pindar -

Rodrigo Alfaro Arancibia

Rodrigo Alfaro Arancibia -

Sven Schreiber

Sven Schreiber