1:37 a.m.

Hi,

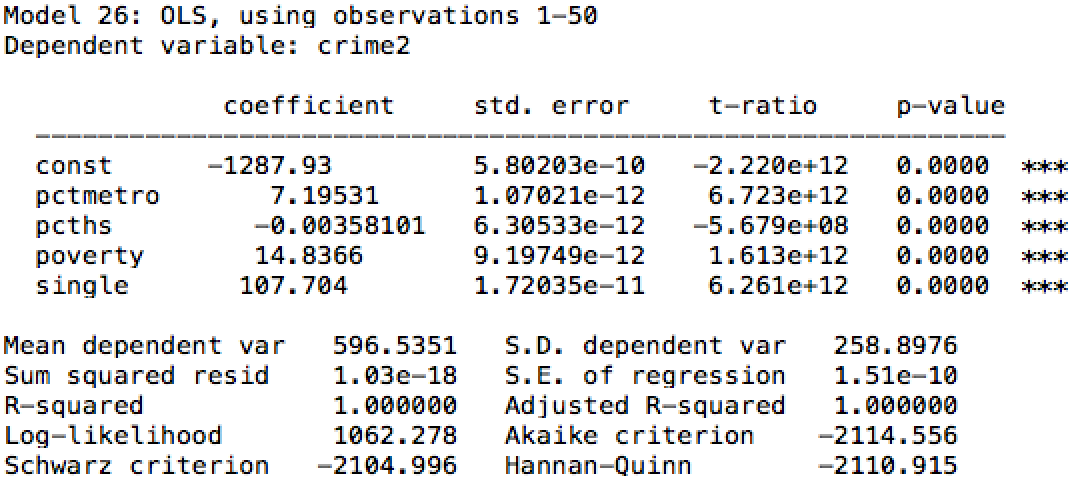

Probably the topic of "How small is really small?" has been already

discussed but I'm still a bit confused.

Now, for the following estimation, Stata considers that std errors are 0

and provides no output. Instead, gretl reports quite small values resulting

in very "optimistic" p-values.

Obviously, the missing F statistic and a R2=1 should provoke doubt and

question the validity of the model...though those *** seem confusing :).

In such circumstances, is there a way to make gretl "judge" that std.errors

are actually 0 and omit t tests?

Best,

Artur

[image: image.png]

{kind=link}

7:55 p.m.

New subject: On near-zero std errors values

Hi,

Probably the topic of "How small is really small?" has been already

discussed but I'm still a bit confused.

On an OLS estimation, where Stata considers that std errors are actually 0

and provides no related output, gretl instead reports quite small values,

kind of e-10, resulting in very "optimistic" p-values.

Obviously, gretl's missing F statistic and a R2=1 should provoke doubt and

question the validity of the model...yet those *** for the p-values seem

confusing :).

In such circumstances, is there a way to make gretl

"judge" that std.errors are actually 0 and discard t tests?

Best,

Artur

8:50 p.m.

On Fri, 29 Jan 2021, Artur Bala wrote:

Hi,

Probably the topic of "How small is really small?" has been already

discussed but I'm still a bit confused.

Now, for the following estimation, Stata considers that std errors are 0

and provides no output. Instead, gretl reports quite small values resulting

in very "optimistic" p-values.

Obviously, the missing F statistic and a R2=1 should provoke doubt and

question the validity of the model...though those *** seem confusing :).

In such circumstances, is there a way to make gretl "judge" that std.errors

are actually 0 and omit t tests?

In my opinion, we need to take no such action. Let me explain my point.

The standard errors one see printed by the side of estimated coefficients

are, per se, just descriptive statistics that give you an idea of how

sensitive the objective function (the sum of squares) is to changes in

that parameter. If that number is small, it means that small changes in

that parameter make the model much worse in fitting the dependent

variable. That's what the standard errors are.

That said, you _may_ give them an inferential interpretation and use them

to construct hypothesis tests and confidence intervals, but then, the

burden of correctly interpreting their meaning is on the user. The fact

that many, in the economic profession, have come to the unfortunate habit

of automatically thinking "no stars -> bad, two stars -> good, three stars

-> wow" should not deter us, as authors of a statistical package, from

reporting the statistic in the most precise way possible and refrain from

patronising the user.

-------------------------------------------------------

Riccardo (Jack) Lucchetti

Dipartimento di Scienze Economiche e Sociali (DiSES)

Università Politecnica delle Marche

(formerly known as Università di Ancona)

r.lucchetti(a)univpm.it

http://www2.econ.univpm.it/servizi/hpp/lucchetti

-------------------------------------------------------

9:19 p.m.

Le sam. 30 janv. 2021 à 10:51, Riccardo (Jack) Lucchetti <

p002264(a)staff.univpm.it> a écrit :

On Fri, 29 Jan 2021, Artur Bala wrote:

> In such circumstances, is there a way to make gretl "judge" that

std.errors

> are actually 0 and omit t tests?

In my opinion, we need to take no such action. Let me explain my point.

The standard errors one see printed by the side of estimated coefficients

are, per se, just descriptive statistics that give you an idea of how

sensitive the objective function (the sum of squares) is to changes in

that parameter. If that number is small, it means that small changes in

that parameter make the model much worse in fitting the dependent

variable. That's what the standard errors are.

That said, you _may_ give them an inferential interpretation and use them

to construct hypothesis tests and confidence intervals, but then, the

burden of correctly interpreting their meaning is on the user. The fact

that many, in the economic profession, have come to the unfortunate habit

of automatically thinking "no stars -> bad, two stars -> good, three stars

-> wow" should not deter us, as authors of a statistical package, from

reporting the statistic in the most precise way possible and refrain from

patronising the user.

Thank you Jack! I fully agree with you on the "misuse" of those asterisks

and personally I would

also refrain from suggesting any interpretation to the user.

However, in this precise case, there's obviously something wrong with this

model and if it was to be

consistent, gretl would also need to provide the F-statistic should it be 0

or NA (alongside its p-valeu).

This will be an additional warning to the user that things are not as they

appear to be...

Best,

Artur

1993

days inactive

1994

days old

3 comments

2 participants

participants (2)

-

Artur Bala

Artur Bala -

Riccardo (Jack) Lucchetti

Riccardo (Jack) Lucchetti