[Gretl-users] GARCH results differences

Dear hello,

I run an AR(10)-GARCH(2,2) model just for an example using the included

data file djclose.gdt

I run the following:

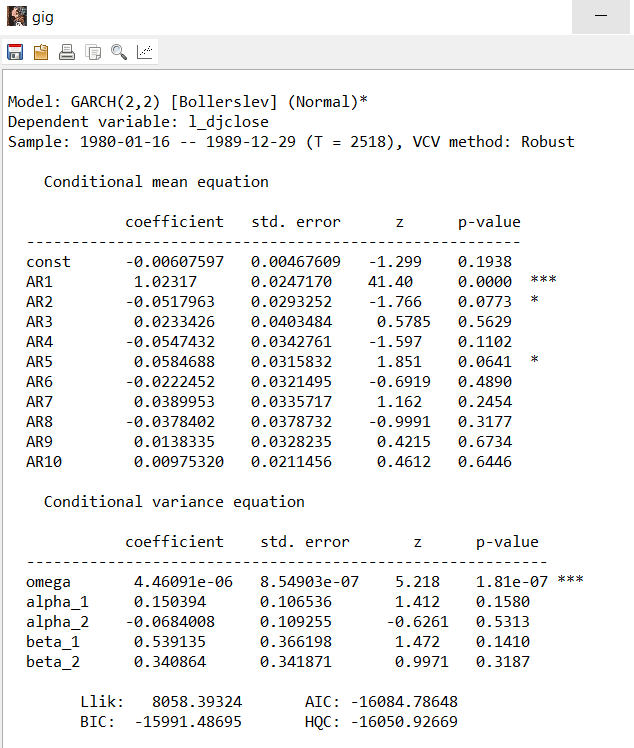

*Model 1:*

Model>Time Series>GARCH Variants and got this:

[image: Inline image 1]

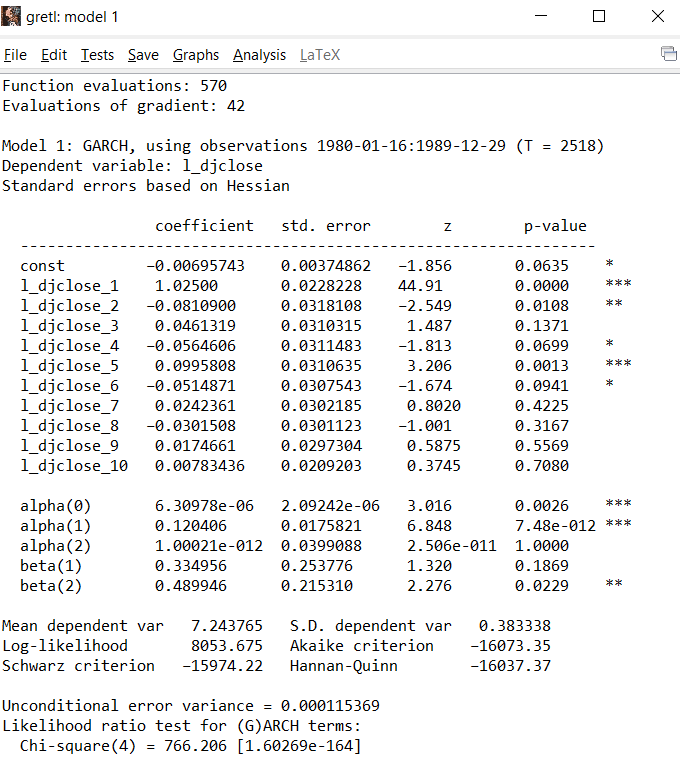

*Model 2:*

Model>Time Series>GARCH and got this:

[image: Inline image 2]

Why do I get so different results on the same data and model? The

results are very different in both the mean equation and the GARCH

part. They are both an AR(10)-GARCH(2,2) in the logs.

Thank you very much,

PG

*Periklis Gogas

<http://www.econ.duth.gr/personel/dep/gkogkas/index.en.shtml>*

Associate Professor

of Economic Analysis and International Economics

Department of Economics, Democritus University of Thrace

Euro Area Business Cycle Network - Fellow

<http://www.eabcn.org/person/periklis-gogas>

The Rimini Centre for Economic Analysis - Fellow

<http://www.rcfea.org/component/option,com_frontpage/Itemid,1/>

The Society for Economic Measurement - Member

<http://sem.society.cmu.edu/home.html>

Institute for Nonlinear Dynamical Inference (INDI) - Charter Fellow

<http://icemr.ru/institute-for-nonlinear-dynamical-inference/>

Το νέο βιβλίο μου: Οικονομικά για μη Ειδικούς

<http://kritiki.gr/product/ikonomika-gia-mi-idikous/>

Attachments:

- attachment.html (text/html — 3.4 KB)

- image.png (image/png — 61.8 KB)

- image.png (image/png — 75.1 KB)

{kind=link}

{kind=link}