4:09 p.m.

Can one assume that the interval in the forecast GUI Analysis option of an

estimated model is a true prediction interval?. If indeed it is, it would

also be useful to be able to graph the prediction interval surrounding the

fitted function values as well as the forecast ones.

Brian J Revell

Professor Emeritus

Harper Adams University , Shropshire

Current Chair of Defra Economic Advisory Panel

Tel 01952 815237

Tel: +44 1952 728153

Mbl +44 7976 538712

University: +44 1952 815235

alt: email: bjrevell(a)harper-adams.ac.uk

9:50 a.m.

Am 09.10.2021 um 18:09 schrieb Brian Revell:

Can one assume that the interval in the forecast GUI Analysis option

of

an estimated model is a true prediction interval?. If indeed it is, it

would also be useful to be able to graph the prediction interval

surrounding the fitted function values as well as the forecast ones.

Sorry, I think you need to define/explain a little more what you mean by

"true prediction interval".

thanks

sven

12:39 p.m.

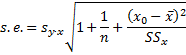

The word "true" was used to draw attention to the distinction between a

prediction interval for a specific forecast/future value of y arising from

a value x0 and a CI for the regression line in relation to the values of x

in the sample.

The standard error differs between former and latter viz

[image: image.png] defines the standard error of a prediction of y given

a specific value of x0 and

[image: image.png] defines the standard error for the values of y from the

values of x underlying the parameter estimate generating y|x

On Sun, 10 Oct 2021 at 10:50, Sven Schreiber <svetosch(a)gmx.net> wrote:

Am 09.10.2021 um 18:09 schrieb Brian Revell:

> Can one assume that the interval in the forecast GUI Analysis option of

> an estimated model is a true prediction interval?. If indeed it is, it

> would also be useful to be able to graph the prediction interval

> surrounding the fitted function values as well as the forecast ones.

Sorry, I think you need to define/explain a little more what you mean by

"true prediction interval".

thanks

sven

_______________________________________________

Gretl-users mailing list -- gretl-users(a)gretlml.univpm.it

To unsubscribe send an email to gretl-users-leave(a)gretlml.univpm.it

Website:

https://gretlml.univpm.it/postorius/lists/gretl-users.gretlml.univpm.it/

{kind=link}

{kind=link}

7:52 a.m.

Am 10.10.2021 um 14:39 schrieb Brian Revell:

The word "true" was used to draw attention to the

distinction between

a prediction interval for a specific forecast/future value of y

arising from a value x0 and a CI for the regression line in relation

to the values of x in the sample.

...

If I interpret you correctly, then "CI for the regression line" would

reflect estimation uncertainty, which is also called parameter

uncertainty. (As opposed to the additinal aspect of innovation

uncertainty in forecasting.)

See the last paragraph of the reference for the "fcast" command (and

perhaps also a corresponding part of the guide) for a description of

what the forecast interval (the standard errors) encompasses; it depends

on the properties of the model. But it is always true that it is _not_

an application of the interval for the regression line in the sense above.

On Sun, 10 Oct 2021 at 10:50, Sven Schreiber <svetosch(a)gmx.net

<mailto:svetosch@gmx.net>> wrote:

Am 09.10.2021 um 18:09 schrieb Brian Revell:

> Can one assume that the interval in the forecast GUI Analysis

option of

> an estimated model is a true prediction interval?. If indeed it

is, it

> would also be useful to be able to graph the prediction interval

> surrounding the fitted function values as well as the forecast ones.

Here I understand you as asking for a graphical representation of the

parameter uncertainty of the estimated regression line. Or perhaps also

to disentangle the various uncertainty components of a forecast. I'm not

sure we have that. Spontaneously I'd say that for the case with more

than one regressor that would involve the same methods and algorithms as

for capturing that aspect in the forecasting case, which is certainly

feasible but not trivial in general. E.g., for the probably most

important case of dynamic forecasts core gretl does not cover parameter

uncertainty. (Basically one would need a bootstrap I think.)

These remarks are all for standard regressions. Since you have worked

with the StrucTiSM package in the past, let me be clear that issues are

somewhat different there. Were you talking about forecasts with StrucTiSM?

cheers

sven

8:28 a.m.

Hi Sven

no I was not using StrucTiSM in this case, but models specified and

estimated with OLS and ARMAX. The post estimation Analysis GUI options

include Forecasts . Exogenous variable projected values are provided for

both OLS and ARMAX variant forecasts The displayed results are

prediction std. error 95% interval So my question relates to

whether the std. error is that of the regression line or the predicted

values, which differs from the regression std. error.

Hope that is clear.

Brian

On Mon, 11 Oct 2021 at 08:52, Sven Schreiber <svetosch(a)gmx.net> wrote:

Am 10.10.2021 um 14:39 schrieb Brian Revell:

The word "true" was used to draw attention to the distinction between a

prediction interval for a specific forecast/future value of y arising from

a value x0 and a CI for the regression line in relation to the values of x

in the sample.

...

If I interpret you correctly, then "CI for the regression line" would

reflect estimation uncertainty, which is also called parameter uncertainty.

(As opposed to the additinal aspect of innovation uncertainty in

forecasting.)

See the last paragraph of the reference for the "fcast" command (and

perhaps also a corresponding part of the guide) for a description of what

the forecast interval (the standard errors) encompasses; it depends on the

properties of the model. But it is always true that it is _not_ an

application of the interval for the regression line in the sense above.

On Sun, 10 Oct 2021 at 10:50, Sven Schreiber <svetosch(a)gmx.net> wrote:

> Am 09.10.2021 um 18:09 schrieb Brian Revell:

> > Can one assume that the interval in the forecast GUI Analysis option of

> > an estimated model is a true prediction interval?. If indeed it is, it

> > would also be useful to be able to graph the prediction interval

> > surrounding the fitted function values as well as the forecast ones.

Here I understand you as asking for a graphical representation of the

parameter uncertainty of the estimated regression line. Or perhaps also to

disentangle the various uncertainty components of a forecast. I'm not sure

we have that. Spontaneously I'd say that for the case with more than one

regressor that would involve the same methods and algorithms as for

capturing that aspect in the forecasting case, which is certainly feasible

but not trivial in general. E.g., for the probably most important case of

dynamic forecasts core gretl does not cover parameter uncertainty.

(Basically one would need a bootstrap I think.)

These remarks are all for standard regressions. Since you have worked with

the StrucTiSM package in the past, let me be clear that issues are somewhat

different there. Were you talking about forecasts with StrucTiSM?

cheers

sven

_______________________________________________

Gretl-users mailing list -- gretl-users(a)gretlml.univpm.it

To unsubscribe send an email to gretl-users-leave(a)gretlml.univpm.it

Website:

https://gretlml.univpm.it/postorius/lists/gretl-users.gretlml.univpm.it/

1619

days inactive

1621

days old

4 comments

2 participants

participants (2)

-

Brian Revell

Brian Revell -

Sven Schreiber

Sven Schreiber