[Gretl-users] GARCH Conversion

Hi all,

I am using Gretl with a class of graduate students and for one of the

assignments they have to estimate the optimum GARCH specification based on

their data. Each student uses different stock prices as the variable in

question.

When they use both options:

1. Model > Time Series > GARCH

2. Model > TIme Series > GARCH Variants

We seldom get results as the vats majority of models do not converge. This

makes it very difficult to use Gretl in class. Why is this? What is the

problem?

The same data with the same specification run and get results in Eviews for

example.

Bellow I have estimated an AR(10) model with an ARCH(1) specification just

to show you the problem.

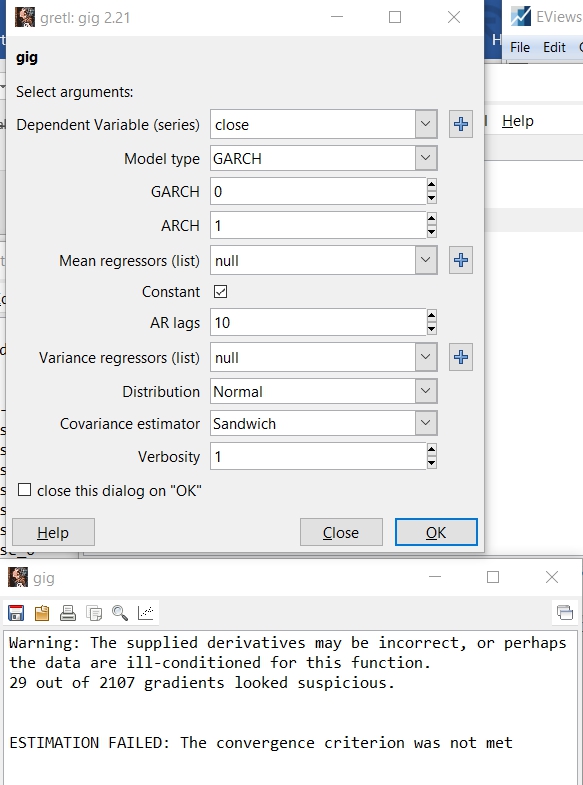

Using Gretl I get this:

(alternative link: http://i64.tinypic.com/23sc5zq.jpg)

[image: screenshot_1895.jpg]

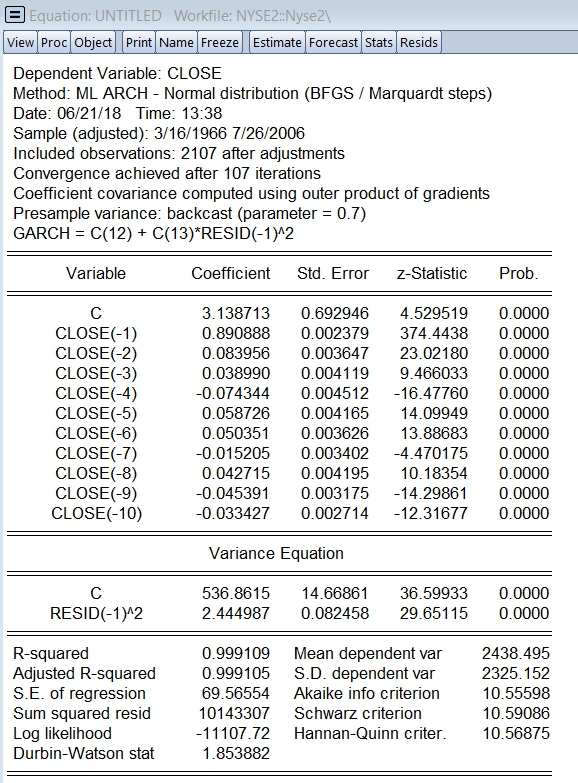

And using Eviews with exactly the same specification and data I get this:

(alternative link: http://i65.tinypic.com/2yv3vj6.jpg)

[image: screenshot_1896.jpg]

And this happens a lot of times with alternative ARCH/GARCH specifications

rendering Gretl impossible to use in class for these types of models.

Any ideas?

PG

*Periklis Gogas

<http://www.econ.duth.gr/personel/dep/gkogkas/index.en.shtml>*

Associate Professor

of Economic Analysis and International Economics

Department of Economics, Democritus University of Thrace

Associate Editor - Journal of Economic Asymmetries

<https://www.journals.elsevier.com/the-journal-of-economic-asymmetries/>

Euro Area Business Cycle Network - Fellow

<http://www.eabcn.org/person/periklis-gogas>

The Rimini Centre for Economic Analysis - Fellow

<http://www.rcfea.org/component/option,com_frontpage/Itemid,1/>

The Society for Economic Measurement - Member

<http://sem.society.cmu.edu/home.html>

Institute for Nonlinear Dynamical Inference (INDI) - Charter Fellow

<http://icemr.ru/institute-for-nonlinear-dynamical-inference/>

Σύγχρονοι Ελληνικοί Μύθοι

<http://www.public.gr/product/syghronoi-ellinikoi-mythoi/prod9040056pp/?so...

- το νέο μου βιβλίο

{kind=link}

{kind=link}

Attachments:

- attachment.html (text/html — 4.7 KB)

- screenshot_1895.jpg (image/jpeg — 177.8 KB)

- screenshot_1896.jpg (image/jpeg — 421.4 KB)

{kind=link}

{kind=link}