[Gretl-devel] Bug in Exponential Smoothing

Hello Devs,

I believe there is a bug in the Exponential Smoothing code. Using the

example from Makridakis, Wheelwright, Hyndman, "Forecasting Methods and

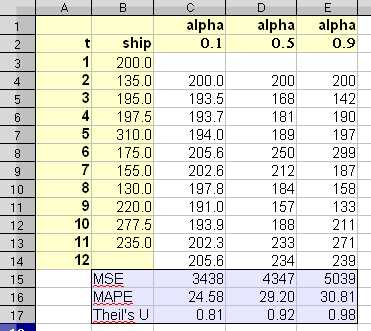

Applications," 3e, table 4-3 on page 151, we should get,

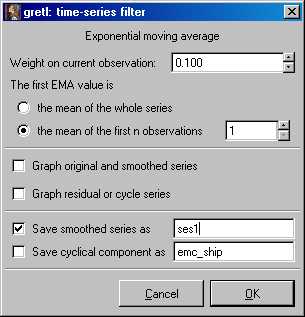

When running the same in GRETL using

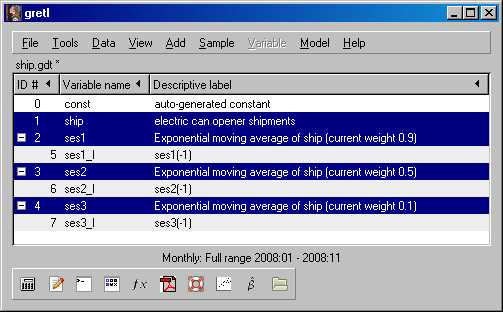

for each series, we get

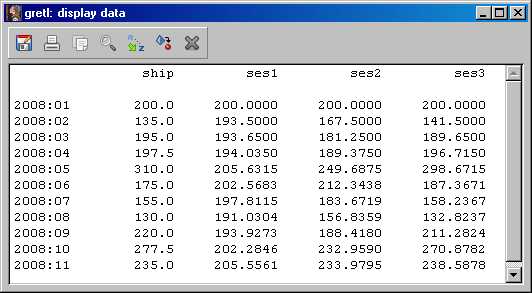

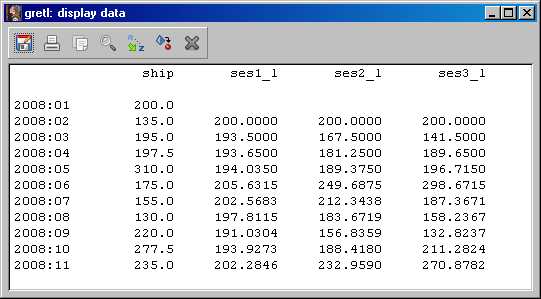

When displayed we get,

To get the same MSE as Makridakis we need,

? printf "MSE for SES1 is: %9.3f\n", sum((ship-ses1(-1))^2)/10

MSE for SES1 is: 3438.332

? printf "MSE for SES2 is: %9.3f\n", sum((ship-ses2(-1))^2)/10

MSE for SES2 is: 4347.237

? printf "MSE for SES3 is: %9.3f\n", sum((ship-ses3(-1))^2)/10

MSE for SES3 is: 5039.368

The calculated EMAs are correct, but need to be lagged.

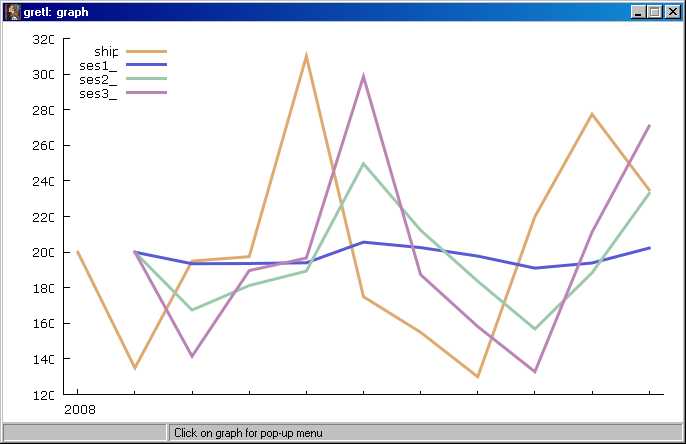

Which provides a graph that matches their figure 4-7

--Peter

Attachments:

- attachment.html (text/html — 1.8 KB)

- moz-screenshot-34.jpg (image/jpeg — 28.0 KB)

- moz-screenshot-35.jpg (image/jpeg — 16.3 KB)

- moz-screenshot-36.jpg (image/jpeg — 29.2 KB)

- moz-screenshot-37.jpg (image/jpeg — 33.9 KB)

- moz-screenshot-38.jpg (image/jpeg — 32.4 KB)

- moz-screenshot-39.jpg (image/jpeg — 25.9 KB)

- gretl-expmovavg.pdf (application/pdf — 99.7 KB)

- chapter4-exponentialsmoothing1-ses.ods (application/vnd.oasis.opendocument.spreadsheet — 30.3 KB)

- ship.gdt (application/x-gretldata — 817 bytes)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}